22 / 100

22 / 100

August

2019

HYDROCARBON

ENGINEERING

20

market area. Some of them decided to close their refineries

entirely. Thus, not only did Australia fail to become a major

export refining hub in the region, the refining industry

began to shrink. The domestic market was limited, and

gasoline demand was forecast to decline. Domestic crude

oil production was declining as well, pointing to a future of

imported crude feedstocks. The Department of

Environment and Energy reported that the percentage of

indigenous refinery inputs fell to 20.3% in 2017 – 2018.

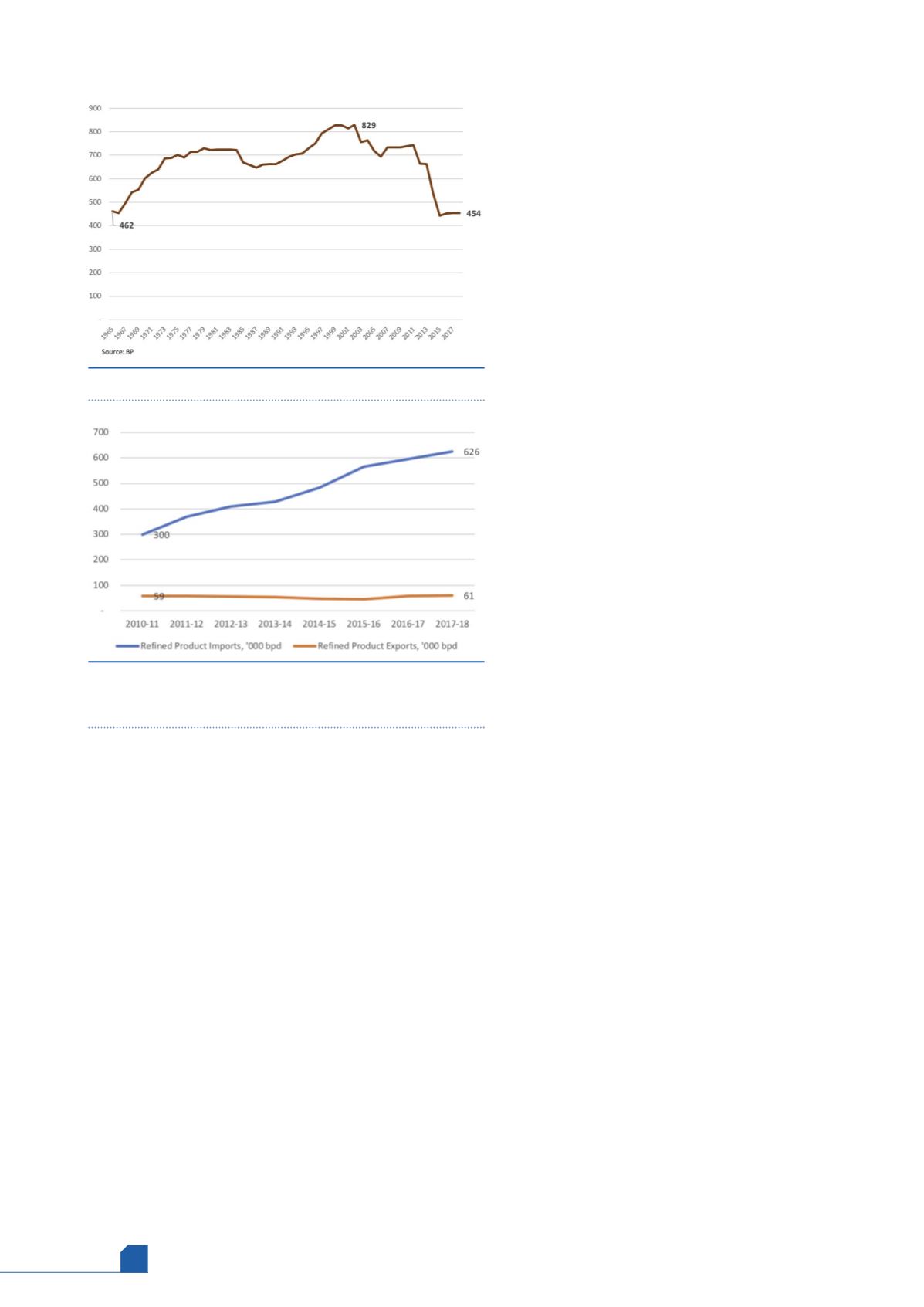

Figure 5 traces how Australia’s crude refining capacity

peaked at 829 000 bpd in 2002, dropped below

700 000 bpd in 2006, and collapsed to 452 000 bpd in 2016

before creeping back slightly to 454 000 bpd in 2018.

Caltex closed its Kurnell refinery at the end of 2014. BP

closed its Bulwer Island refinery in 2015. Shell already had

begun to divest itself of refinery assets in many parts of

the globe, and this included Australia. Shell announced

that it would convert its Clyde refinery to a product

terminal in 2013, and Shell sold its Geelong refinery to the

oil trading company Vitol in 2014. This refinery is now

known as the Viva Vitol refinery.

Today, only four refineries remain in operation: BP

Kwinana, Caltex Lytton, ExxonMobil Altona, and Vitol Viva

Geelong. These refineries share a number of similarities.

They are mid-sized, they rely on catalytic cracking as their

central upgrading technology, and they use a

combination of catalytic reforming, alkylation, and

isomerisation for octane provision. The refineries are

oriented toward gasoline. Australian refinery output in

FY 2017 – 2018 was 39.8% gasoline, 32% diesel, 13.3% jet

fuel, 2.7% fuel oil, 3.4% LPG, and 8.7% other products.

Australia now depends on imports for most of its

needs. Diesel sales in FY 2017 – 2018, for example,

were 486 800 bpd. Refinery production was only

158 300 bpd, less than 33% of demand. Domestic

refineries satisfied 62% of the gasoline market.

Gasoline production in 2017 – 2018 was 197 000 bpd,

against sales of 316 500 bpd.

Refined product exports dwindle,

imports grow

Australia’s refined product exports have fallen, while

imports have risen. As Figure 6 illustrates, refined

product imports have more than doubled from

300 000 bpd in 2010 – 2011 to 626 000 bpd in

2017 – 2018. Looking back further in history, in

2001 – 2002, Australia imported only around

74 000 bpd of refined products. The wave of refinery

closures brought a steady increase in imports.

Middle distillate imports have grown swiftly. In

FY 2001 – 2002, middle distillate imports were only

26 000 bpd. In FY 2007 – 2008, this jumped to

160 700 bpd. By 2017 – 2018, diesel imports had

expanded to 346 800 bpd. In total, Australia’s imports

of refined product increased at rates averaging 11.1%

per year between 2010 – 2011 and 2017 – 2018. This has

amounted to an increase of nearly 325 500 bpd of

refined products in just seven years.

Product exports have fallen and stagnated in

recent years. In 2001 – 2002, product exports were

114 000 bpd. This fell to 58 600 bpd in 2010 – 2011, and

product exports averaged 60 900 bpd in 2017 – 2018.

Exports exclude international bunkering, which were

reported at 38 600 bpd in 2017 – 2018. Most of this

(33 650 bpd) was aviation fuels.

Most of Australia’s product exports are LPG. In

FY 2017 – 2018, LPG accounted for 65% of the 60 900 bpd

exported. Most of this is shipped to Asia-Pacific

destinations such as Japan, South Korea, Indonesia, and

Singapore, but cargoes travel as far as Africa.

Gasoline and diesel exports are now quite small: in

FY 2017 – 2018, gasoline exports were 2600 bpd, and diesel

exports were a mere 1500 bpd.

Australia is a key supplier of fuel to some of the

smaller markets in the Pacific, including the Solomon

Islands, New Caledonia, Papua New Guinea, Vanuatu, Fiji,

French Polynesia, and Samoa. Although the amounts are

small, in many cases Australia is the sole source of supply

for these islands, and the export avenues therefore have a

greater significance than the volumes suggest.

Conclusion: can Australia reduce its

carbon intensity as pledged?

There is no doubt that fossil energy resources have

contributed enormously to the Australian economy.

Figure 6.

Australia’s refined product imports are growing,

exports stagnating (‘000 bpd). Source: Department of

Environment and Energy.

Figure 5.

Australia’s refinery capacity (‘000 bpd). Source: BP.