16 / 76

16 / 76

July

2020

HYDROCARBON

ENGINEERING

14

peak in the second quarter, with a gradual return to normality in

the second half of 2020.

In stark contrast to the ADB, the IMF along with many

private economists are nervously referencing the Great

Depression in their analyses.

As most of developing Asia has yet to see a peak in

COVID-19’s spread, it is the ADB that may have to soon

downgrade its forecast for Southeast Asia’s economies.

With the Brent crude price plunging from an average

US$66/bbl in 2019 to under US$20/bbl in late April, the region’s

energy producers Brunei, Indonesia, Malaysia and Vietnam could

have their oil and gas export earnings slashed by as much as 70%

this year. The US benchmark crude, West Texas Intermediate

(WTI), fell to a new record low of minus US$40/bbl on 20 April.

For net energy importers Cambodia, Laos, Myanmar,

Singapore, Philippines and Thailand, the benefit of cheaper oil

and gas will be offset by the shock of sharply weaker exports

and lower economic growth.

Southeast Asia’s fuels trade deficit to

continue

Southeast Asia’s fuels trade will likely remain in deficit in the

coming years as the region’s energy demand continues to grow

while its domestic oil reserves decline.

For 2018, the latest data available, the World Bank found

that eight of the region’s ten countries spent a total of

US$213.3 billion on fuel imports while earning US$155.9 billion in

exports. Their combined net position was a loss of

US$57.4 billion.

The World Bank did not include Laos and Vietnam as their

data was not available for 2018.

Only three of the region’s economies registered a surplus in

their fuels trade that year, thanks to the Brent crude price

averaging US$71/bbl, the highest since 2014.

Indonesia had the largest fuels trade surplus of

US$10.4 billion in 2018, which could be the peak given the sharp

drop in energy prices since then. At the same time, the country’s

oil consumption grew 5.2% year-on-year to 1.785 million bpd in

2018 while its proved oil reserves stagnated at 3.2 billion bbl,

according to BP.

The fuel trade surpluses of Malaysia and Brunei are also set

to decline as the two countries are expanding their downstream

plants, which will raise their domestic consumption of crude

and oil products. Malaysia’s oil consumption grew 2.6%

year-on-year to 814 000 bpd in 2018 while its oil reserves

remained at 3 billion bbl.

Brunei’s new refinery-petrochemical complex, which started

up in late 2019, is expected to operate at capacity from the

second half of 2020.

Majority owned by China’s Hengyi Petrochemical Co. Ltd,

the complex comprises an 8 million t (or 160 000 bpd) refinery

that will produce fuel and refined products mostly for export to

neighbouring countries. It also supplies feedstock directly into

the integrated petrochemicals plant, which has the capacity to

produce 1.5 million tpy of paraxylene and 500 000 tpy of

benzene for export to China.

Singapore registered the region’s biggest net fuel trade

deficit of US$33.9 billion as it diverted more of its crude intake

and refined products output for domestic consumption.

Refining margins to “remain depressed”

Southeast Asia’s fast-growing downstream oil sector will face

another difficult year given the continuing uncertainty over the

COVID-19 pandemic and the worsening state of US-China ties.

US ratings agency Moody’s set the tone at the start of 2020

with a bearish outlook on Asia’s downstream refining and

petrochemicals business. That outlook is likely to be further

downgraded.

Referencing the refining margins out of Singapore, the

industry’s benchmark for the region, Moody’s said it expected

continued weakness in the sector in Asia.

Refining margins and petrochemical spreads would “remain

depressed in 2020”, it predicted.

From an average US$6/bbl in 2017 and 2018, Moody’s said

Asia’s refining margins slumped to US$3.70/bbl in 2019, even

turning negative in December. This trend will likely continue

amid the weakening demand for fuels in Asia for the rest of

2020.

“The economic slowdown in the region that contributes to

the low spreads is unlikely to reverse sharply during 2020,” it said.

Philippines’ oil industry headed for

sharp downturn

The Philippines’ oil industry is bracing for its worst year in over a

decade as the nation’s fuels consumption is expected to plunge

in line with global trends.

As an early warning sign, Luzon Island, home to half the

country’s population of 110 million, reported an immediate 30%

collapse in electricity consumption following a region-wide

lockdown on 15 March to combat the spread of COVID-19.

Luzon, on which the capital city of Manila is located, is also the

country’s main economic engine.

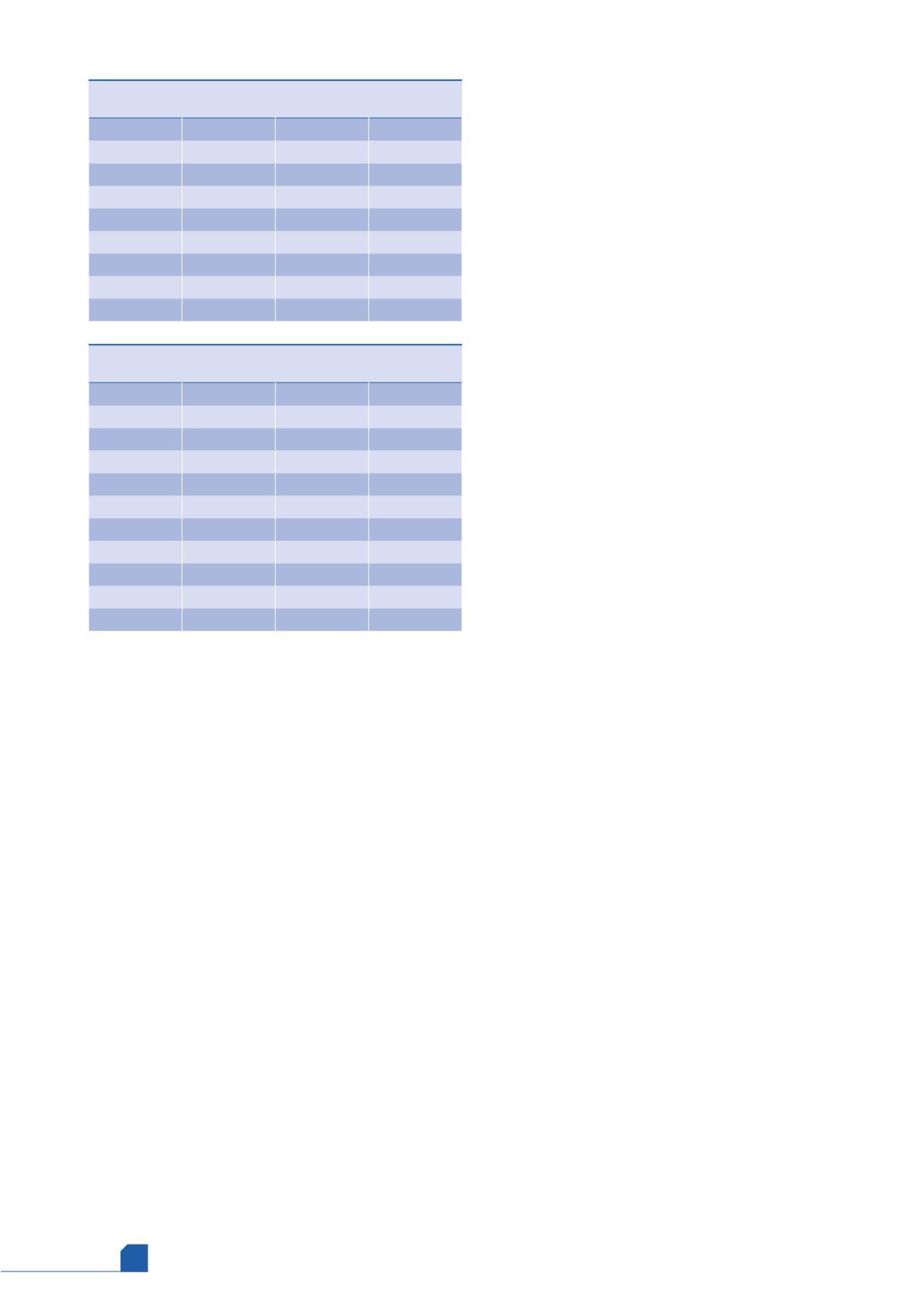

Table 1.

Southeast Asia’s fuels trade, US$ billion,

2019 (source: World Bank)

Export

Import

Balance

Brunei

6.0

0.3

5.7

Indonesia

42.0

31.6

10.4

Malaysia

38.5

33.6

4.9

Myanmar

3.6

4.0

-0.4

Philippines

1.1

13.9

-12.8

Singapore

54.0

87.9

-33.9

Thailand

10.7

42.0

-31.3

Total

155.9

213.3

-57.4

Table 2.

ADB forecast for Southeast Asia’s GDP

growth, %

2019

2020

2021

Brunei

3.9

2.0

3.0

Cambodia

7.1

2.3

5.7

Indonesia

5.0

2.5

5.0

Laos

5.0

3.5

6.0

Malaysia

4.3

0.5

5.5

Myanmar

6.8

4.2

6.8

Philippines

5.9

2.0

6.5

Singapore

0.7

0.2

2.0

Thailand

2.4

-4.8

2.5

Vietnam 7.0

4.8

6.8